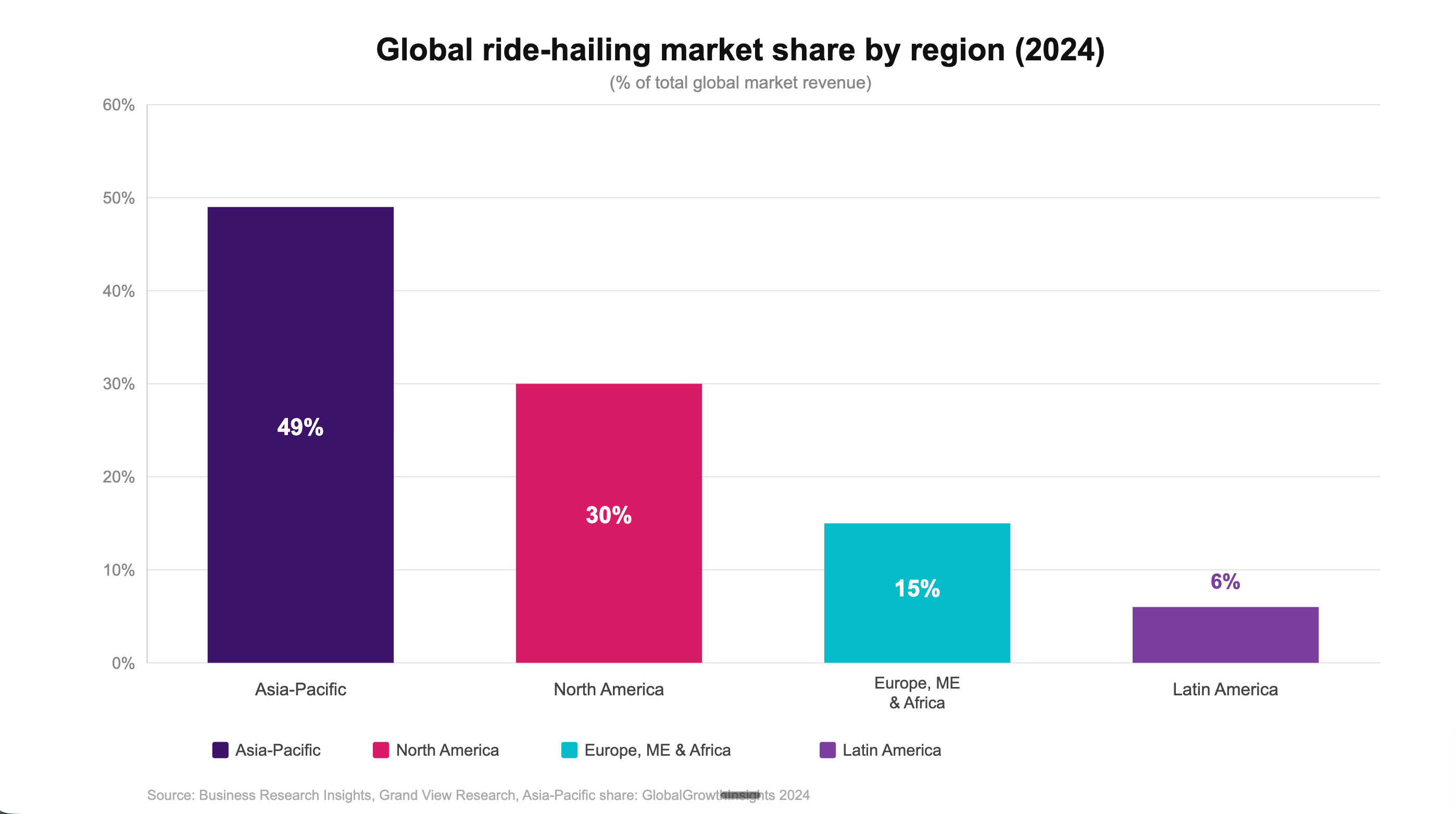

The ride-hailing industry is worth roughly $188–194 billion in 2026. That's not a niche market anymore. More than 2.5 billion people used a ride-hailing service at least once last year, and the average day sees 120 million ride requests globally.

Uber started it all in 2009 under the name UberCab. It still dominates, but the field it opened has matured into something much bigger. Today there are strong, specialized players across every continent, many of whom handle things Uber won't touch, regions it doesn't reach, or price points it won't match.

Here's what the competitive map actually looks like in 2026.

1. Uber

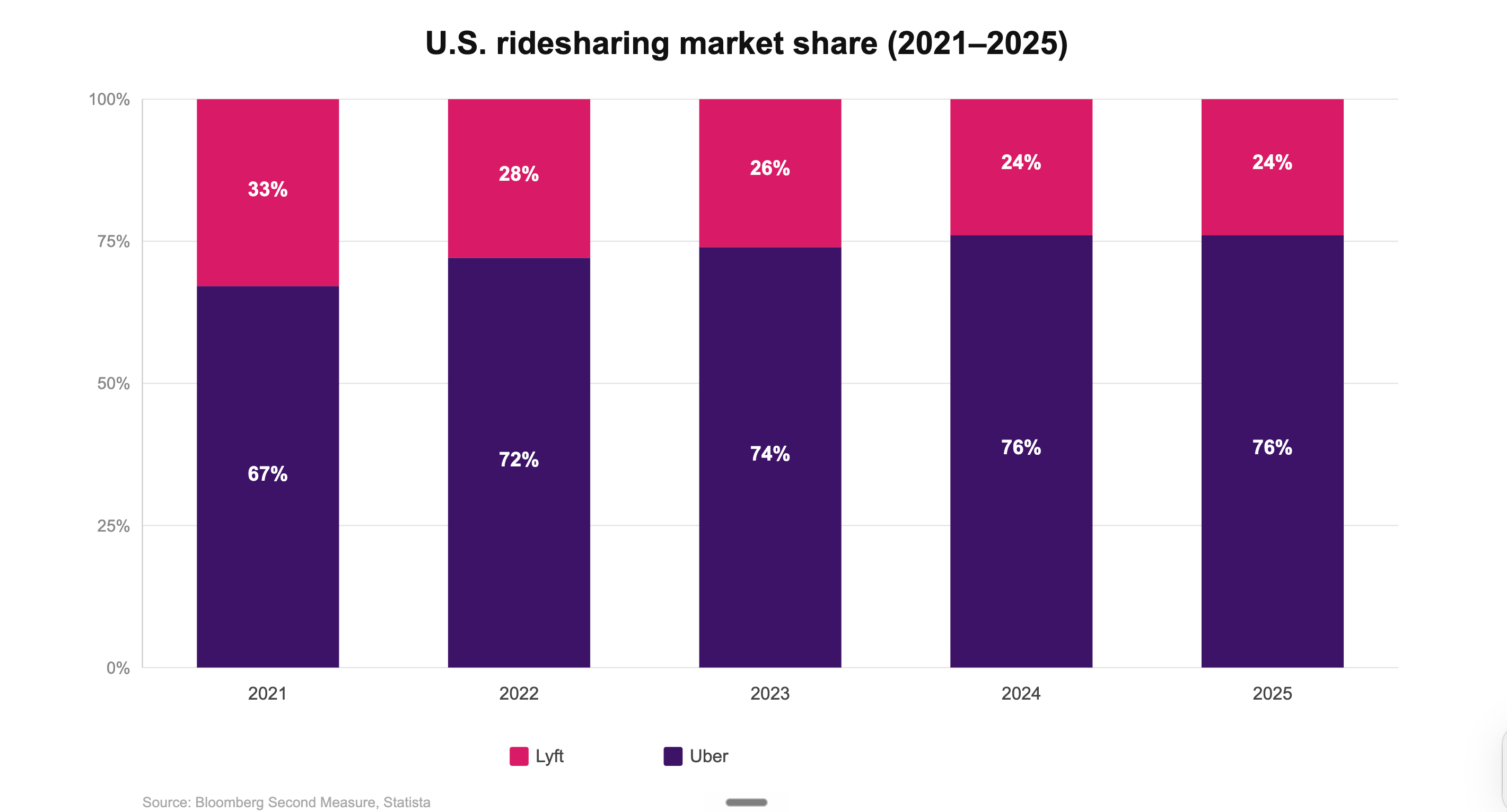

The benchmark everything else is measured against. Uber has 202 million monthly active users across 70 countries, with 42 million trips and deliveries completed every day. In the US, it holds a 76% market share. In FY2025, it delivered $193 billion in gross bookings.

What it gets right: global coverage, a mature driver network, and a product that has added Uber Eats, Uber Freight, and Uber Transit without losing the core experience.

The weak point most people know but rarely say out loud: surge pricing. Demand spikes push fares up sharply, and that erodes driver income consistency and customer loyalty at the same time.

Key features:

- Real-time trip tracking

- Scheduled rides

- Multiple vehicle tiers (UberX, Comfort, Black)

- Unlimited drop-off points

- In-app payment with saved preferences

Available in 70+ countries and 10,000+ cities.

2. Lyft

Lyft is the US market's second-largest player, with roughly 23% of American rides. It launched in 2012 as a peer-to-peer ridesharing service and has since added taxi-hailing, bike share, and scooters. The product is built exclusively for the US and Canada.

It's narrower than Uber by design. No freight, no grocery delivery. The tradeoff is a simpler, cleaner experience that many riders prefer.

Key features:

- Standard and priority pickup options

- Lyft Pink subscription for members

- Driver and rider ratings

- Scheduled rides

- Integration with public transit info in select cities

Available in the US and Canada.

3. Bolt

Bolt is probably the biggest story in European ride-hailing over the last four years. The Estonian company now operates in 50 countries and 600 cities with over 200 million users. As of August 2025, it's valued at €7.4 billion.

Its main edge over Uber in European markets: pricing. Bolt consistently runs 15–20% cheaper. That gap compounds quickly for frequent riders and price-sensitive markets across Eastern Europe and Africa.

Key features:

- Lower base fares vs. Uber in most markets

- Bolt Food delivery in select cities

- Electric scooter and e-bike rentals

- Scheduled rides

- Business accounts

Available in Europe, Africa, Middle East, and Latin America.

4. DiDi

DiDi is the world's largest ride-hailing company by trip volume: 30+ million rides completed daily. It started as a taxi-hailing service in China in 2012, eventually absorbed its main Chinese competitors, and now operates in 14+ countries across Latin America, Eastern Europe, and Oceania.

Its safety infrastructure is worth noting. DiDi runs AI-powered monitoring that tracks both driver and passenger behavior during rides, with one-tap emergency assistance built into the core app.

Key features:

- Private rides, carpooling, taxis, chauffeurs, and buses in one platform

- Separate driver and rider apps

- AI safety monitoring

- Business accounts

- DiDi Express (standard), DiDi Premium (higher-end vehicles)

Available in China, Brazil, Mexico, Australia, New Zealand, Russia, Japan, South Africa, and more.

5. Grab

Grab holds a 73% market share in Southeast Asia, which makes it one of the most dominant regional players anywhere in the world. It launched in 2011 as GrabTaxi and has since grown into a super app covering food delivery, hotel bookings, financial services, and digital payments on top of rides.

What makes it worth covering specifically: the transport options. High-end cars, motorcycles, tuk-tuks (in Thailand), and GrabFamily vehicles with child seats are all available depending on the country. No other operator comes close to that level of localization.

Key features:

- Ride types tailored per country (cars, bikes, tuk-tuks, shuttles)

- GrabFood, GrabMart, hotel booking in one app

- Cash payment option (crucial in cash-heavy SE Asian markets)

- GrabCare fleet for healthcare workers

- Subscription rewards program

Available in Singapore, Malaysia, Thailand, Philippines, Vietnam, Indonesia, Cambodia, and Myanmar.

6. InDrive

InDrive does something no other major ride-hailing app does: lets passengers name their price. The rider proposes a fare, the driver accepts, declines, or counters. That single mechanic changes the entire dynamic.

The result is a very different user experience, particularly in markets where fixed surge pricing feels punishing. InDrive has been downloaded over 400 million times and has held the #2 global spot in ride-hailing app downloads for four consecutive years.

Key features:

- Fare negotiation between rider and driver

- No surge pricing

- Intercity rides

- Courier delivery

- Financial services in select markets

Available in Latin America, Africa, Middle East, South Asia, and Central Asia.

7. Ola

Ola is the dominant ride-hailing platform in India, serving 250+ million users across 250+ cities. Beyond India, it operates in the UK, Australia, and New Zealand. The vehicle range is part of what makes it work in Indian markets: autos (rickshaws), bikes, and shared rides alongside standard cars.

Ola Electric, the company's EV arm, has been expanding its fleet of electric scooters in Indian cities, which ties the ride-hailing product to a broader mobility play.

Key features:

- Auto (rickshaw), bike, and standard car options

- Ola Money in-app wallet

- Ride-sharing (pooled rides)

- Outstation and rental rides for multi-hour use

- SOS emergency button

Available in India, UK, Australia, and New Zealand.

8. BlaBlaCar

BlaBlaCar operates differently from every other app on this list. It's built for intercity travel, not urban rides. Drivers with empty seats post upcoming trips; passengers pay to join and share the fuel cost. The model handles the London–Paris or Madrid–Barcelona type of journey rather than a 10-minute city hop.

The platform has 100 million members across 22 countries. In markets with expensive rail tickets or limited bus frequency, it fills a real gap. It's not a Uber alternative for daily commutes. It's a category of its own.

Key features:

- Long-distance carpooling with verified drivers

- Bus booking in select markets (BlaBlaBus)

- Flexible departure points along routes

- Carbon footprint estimate per trip

- Review system for both drivers and passengers

Available in Europe, India, Brazil, Mexico, and more.

What the market tells you about building one

Uber's model has been copied hundreds of times. Most copies failed. The ones that survived did it by solving a specific problem Uber didn't: cheaper fares in a specific region (Bolt), fare negotiation in price-sensitive markets (InDrive), super-app depth in a single geography (Grab), or a completely different trip type (BlaBlaCar).

The technical architecture is well-understood at this point. Real-time location tracking, dynamic matching, in-app payments, driver and rider verification, and rating systems are table stakes. What separates the winners isn't the feature set. It's the depth of localization and the operational model around it.

We in Brocoders have built platforms in this space and seen what actually makes ride-hailing products work at scale. If you're building in mobility or on-demand services, talk to us about the architecture decisions that matter.

FAQ

Uber, by most measures. It has 202 million monthly active users across 70 countries and handles around 42 million trips and deliveries per day. By download volume, InDrive has held the #2 global spot for four years running, which tells you it's reaching markets where Uber doesn't compete.

Bolt. It runs 15–20% cheaper than Uber across most European and African markets. The gap is most noticeable in Eastern Europe, where Bolt has built a dominant position over the past few years.

InDrive doesn't use surge pricing. Instead, the rider proposes a fare and the driver accepts or counters. It's a different model entirely, and it works well in price-sensitive markets where algorithmic pricing feels unpredictable.

Grab. It holds a 73% market share across the region and supports ride types that no Western app comes close to: tuk-tuks, motorbikes, GrabFamily, and cash payments. It also handles food delivery, hotel bookings, and financial services in one app.

BlaBlaCar. It's not designed for urban rides at all. The model connects drivers making an intercity journey with passengers who want to share the cost. It's active across Europe, India, Brazil, and Mexico, and it's significantly cheaper than rail or bus on many routes.

No. Uber operates in 70 countries and 10,000+ cities, which is vast, but there are major gaps. China (DiDi dominates), most of Southeast Asia (Grab), India (Ola), and parts of Africa (Bolt, InDrive) either blocked Uber from operating or saw local competitors outcompete it before it could establish a foothold.

The standard model is a commission on each fare, typically 20–30% of the trip cost. Some apps run subscription tiers (Lyft Pink, Uber One) that offer discounts in exchange for monthly fees. Delivery and freight services add separate revenue streams. InDrive's fare-negotiation model shifts some of that commission structure, taking a smaller flat fee rather than a percentage.

Ride-hailing means booking a dedicated driver for your trip (Uber, Bolt, DiDi). Ridesharing means sharing a vehicle with strangers who are going the same direction (BlaBlaCar, InDrive's intercity product, carpooling features within Grab). The terms get used interchangeably in the press, but the underlying model is different.