AI is increasingly changing how enterprise software gets bought, and founders are scrambling to figure out what that means for the product they're building. It's a daunting task to decide whether "SaaS" is even the right word anymore, but knowing what's actually changing, not just what the headlines say, can spare you a rebuild eighteen months from now.

Demand for a clear answer has exploded, yet it's a relatively new question, especially given how fast the pricing and spend numbers keep moving. From founders rewriting pitch decks to CTOs re-architecting a live product, everyone building software right now is carrying a decision they didn't have three years ago. Choosing whether to build, price, and position a product as SaaS or as an AI-native product is becoming a critical call, and founders are increasingly tasked with getting that shape right before the market decides it for them.

Gartner and Deloitte, the two firms putting real numbers on this shift, can help clarify where the actual risk sits. Agentic AI puts $234 billion, roughly 20% of enterprise SaaS spending, at risk by 2030, according to Gartner, as agents start acting on business systems directly instead of a person clicking through a screen to get the same job done. "You are no longer buying software primarily for people," says George Brocklehurst, managing vice president at Gartner. "You are increasingly buying it for agents." Once the agent is the user, per-seat pricing and a polished interface stop being what you're paying for.

Deloitte's read on the same shift lands somewhere calmer. "The reality is far more nuanced" than the SaaSpocalypse headlines suggest, says Ayo Odusote, Deloitte's software and platforms leader. His firm expects a blend: AI-native challengers taking the simpler workflows, incumbents bolting agents onto what they already sell, not a clean kill of one side by the other. Brocklehurst, asked directly whether SaaS is dying, called it a metamorphosis instead. SaaS won't be destroyed. It will show up in a different shape.

That's the actual question sitting on your desk, not whether to delete the word "SaaS" from your deck. What shape should your product take, and how should you price it, so it still makes sense past 2027? That's what this article answers.

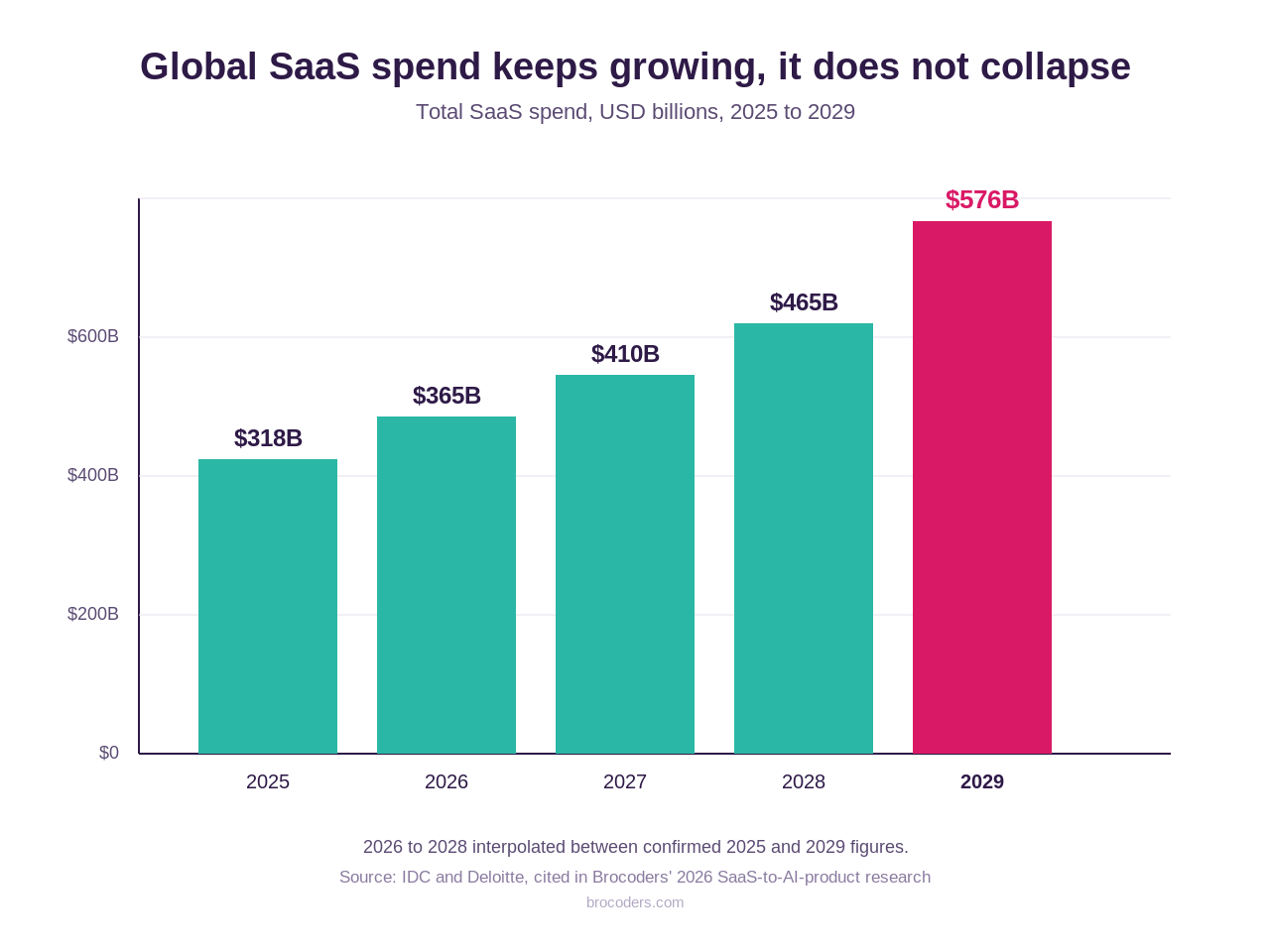

TL;DR: SaaS isn't dying, it's being renamed and re-architected, and global SaaS spend is still growing toward $576 billion by 2029. The real decision isn't the label. It's three concrete checks: positioning, pricing, and shape. We walk through each one, show what we're actually shipping and what's landing in our inbound requests right now (including a year-over-year Upwork trend and a fresh read of our 2026 CRM), look at what Y Combinator's own 2026 batches confirm, and give you a ten-minute self-check to run before you brief anyone.

Is SaaS actually dead in 2026?

No. What's dying is one specific version of SaaS: slow-moving products priced per seat, built on long feature cycles, selling workflow capture that an AI agent can now do directly. That's a real death. It just isn't the whole category's.

The spend data says so plainly. Global SaaS spend is projected to grow from $318 billion in 2025 to roughly $576 billion by 2029, according to IDC and Deloitte. Vertical SaaS alone grows from $133.5 billion to $194 billion over the same window, according to an analysis of the B2B SaaS market. That is not a market in collapse.

What actually changed: pricing is breaking, work is shifting from tools to agents, and vertical beats horizontal. Gartner-cited pricing analysis puts 40% of enterprise SaaS spend shifting to usage, agent, or outcome pricing by 2030. IDC found vertical AI growing at a 36.5% CAGR versus 18.9% for general-purpose tools. Bain's 2026 agentic AI benchmark found agentic AI paying back in 4.1 to 9.3 months depending on function, which is why buyers now accept outcome pricing: the math closes fast enough to risk it.

If you want the full breakdown of the forces driving this shakeout, including why per-seat pricing specifically is the thing breaking, we wrote a longer piece on it: the SaaS apocalypse explained. This article picks up where that one leaves off: given that SaaS isn't dying but is being renamed and re-priced, what should you actually build?

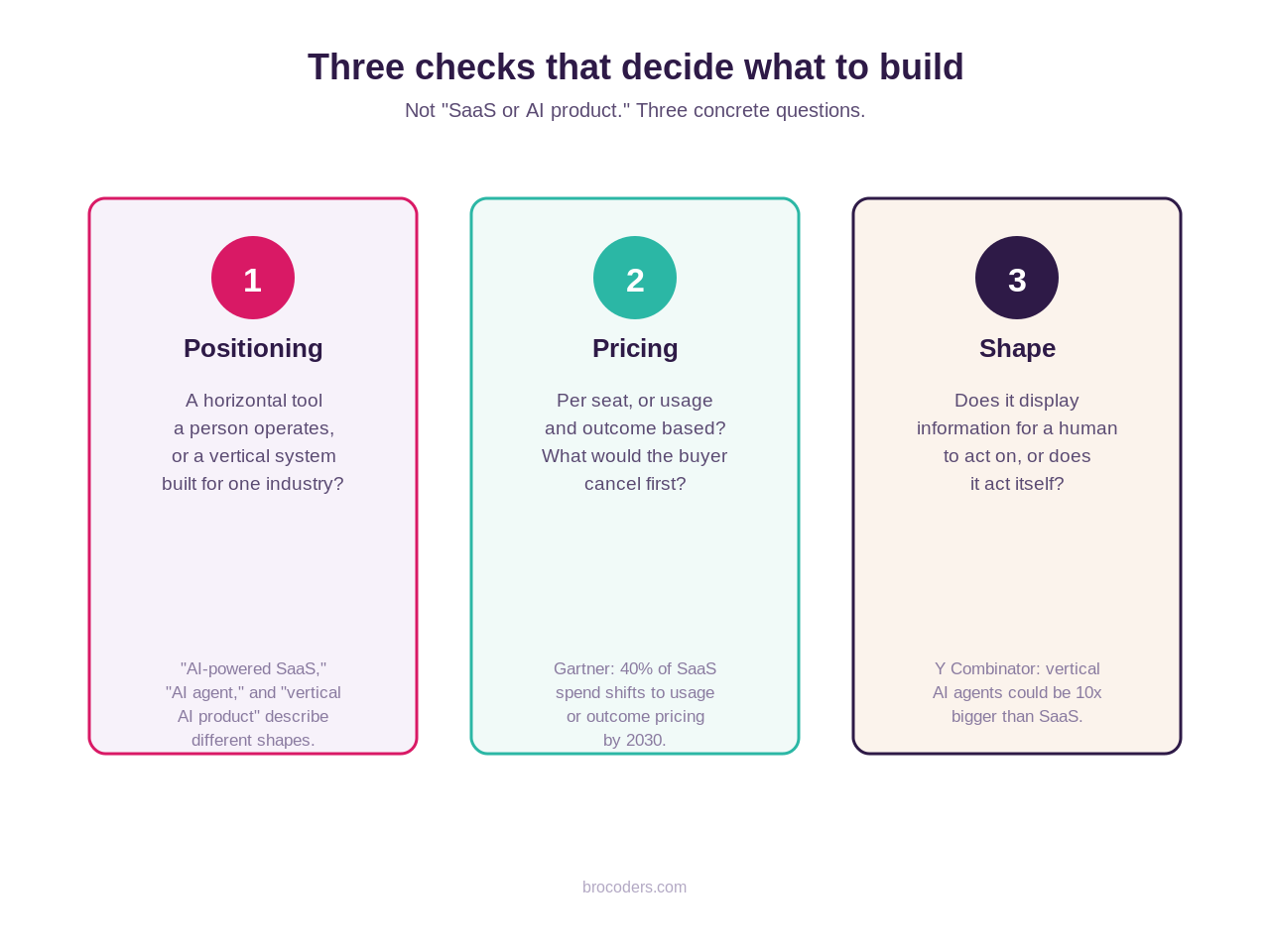

Three checks that actually decide what to build

Forget the label entirely for a minute. Three checks tell you what you're actually building, and each one has a concrete answer you can write down today.

Check 1, positioning. Are you calling this a SaaS, or an AI-native product for one industry? Not a branding choice. A test of whether you're building a horizontal tool humans operate, or a vertical system that does the work itself. "AI-powered SaaS," "AI agent," and "vertical AI product" are not synonyms, they describe different shapes.

Check 2, pricing. Per seat, or usage and outcome based? If ten users need ten licenses, you're on the old model, and that 40% pricing shift means you're pricing against a shrinking share of the market by 2030. If one workflow completed is what the customer pays for, you're already positioned for where enterprise buyers are moving.

Check 3, shape. Does your product display information for a human to act on, or does it act? A dashboard that shows scheduling conflicts is a tool. An agent that reschedules the technician and texts the customer is doing the work. Y Combinator's read on this, that vertical AI agents could be 10x bigger than SaaS, is really a bet on shape, not on category.

Run your own idea through these three, and you'll usually find you're not choosing "SaaS or AI product" at all. You're choosing how much of each you build starting on day one, versus later.

What we're actually building right now

Instead of arguing the framework in the abstract, look at what it produces in practice, on three fronts: what we've delivered, what's landing in our own inbound requests, and what the wider startup market is doing.

Our own delivered work. Inside our case studies knowledge base, the shift is visible without a market report. Of our most recent 49 delivered or in-progress projects, at least 15 are explicitly AI-labeled outright (an AI accounting automation platform, a traceable-answer support assistant, a multi-agent decision tool, an AI video-to-brief generator, and more), and several others carry AI as a core feature inside a broader SaaS build. Roughly a third of our recent delivered work is AI by design, not by marketing.

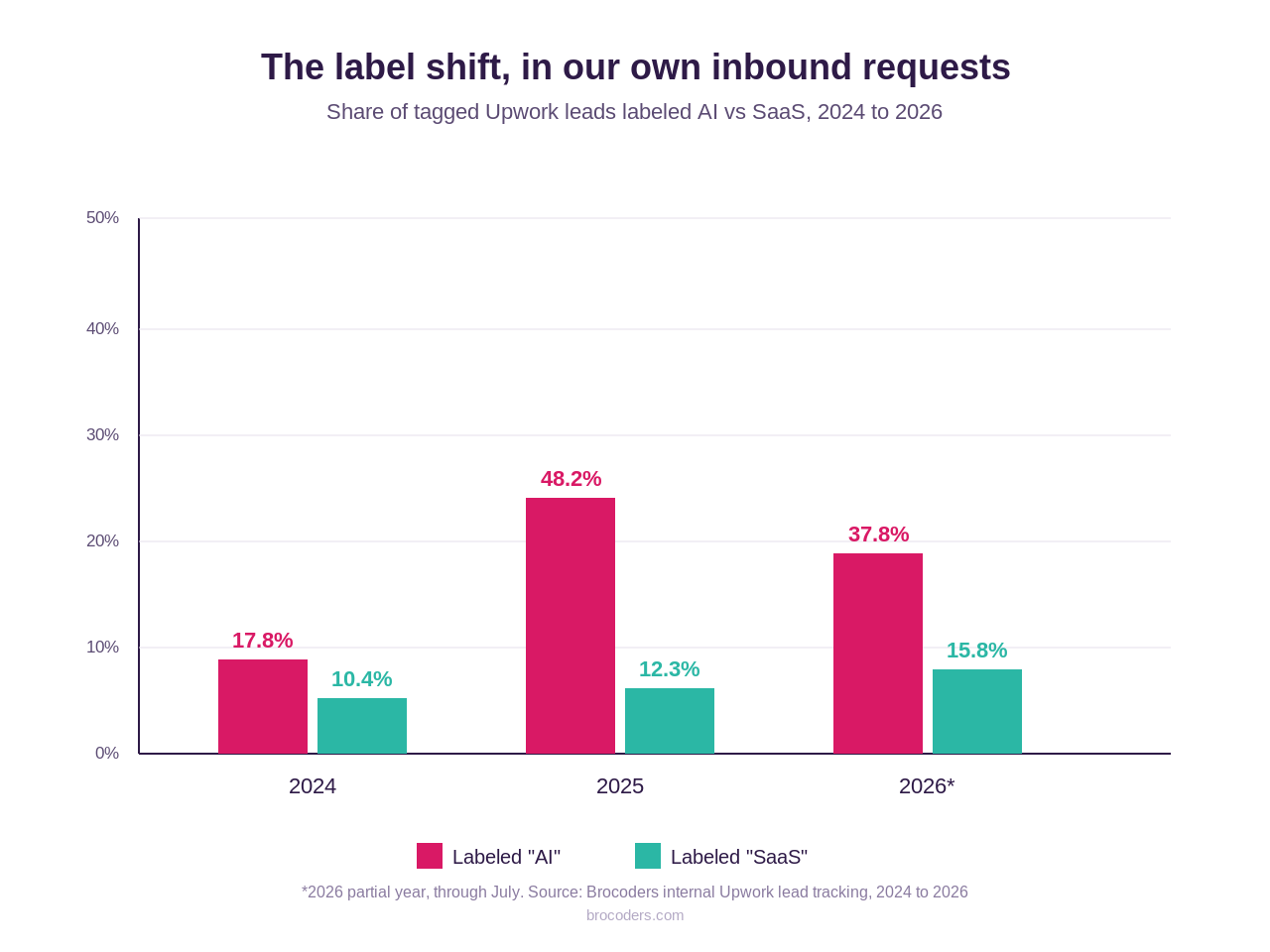

What's coming in the door. We track every Upwork lead we see by category, and the three-year trend line is sharper than any single year on its own.

In 2024, 17.8% of our tagged Upwork leads were labeled AI and 10.4% SaaS. In 2025, AI-labeled demand more than doubled to 48.2%, while SaaS held at 12.3%. Through the first seven months of 2026, AI-labeled demand has settled back to 37.8%, still more than double the 2024 rate, while SaaS-labeled demand kept climbing to 15.8%, its highest share in three years.

Read together, that's not a fad cooling off. It's the label maturing. The 2025 spike looks like the peak of "AI" as a buzzword attached to anything; 2026's numbers look like founders getting more specific about what they're actually asking for, sometimes calling it AI, increasingly comfortable calling it SaaS again once the AI part is assumed rather than sold. Our own 2026 CRM inbound shows the same pattern up close: of the leads that included a real project description this year, several described AI-native builds directly, an AI recommendation engine for interior designers matching style, budget, and material to furniture; a blockchain-plus-AI verification platform for enterprise compliance; an AI-powered non-custodial SaaS bridge with AI-assisted matching, while founders more often called what they were building a "platform" than a "SaaS," even when they meant the latter.

What the wider market is doing. The pattern shows up well beyond our own inbound requests. Y Combinator's 2026 batches were roughly 60% AI companies, up from 40% in 2024, the same direction of travel we're seeing in our own numbers, at a larger scale. YC's own read is that vertical agents are replacing entire SaaS categories, not adding a feature to them.

The sharpest single example of what building the AI-first path looks like is Fielder, our AI orchestrator build: a ServiceTitan-class field service platform generated from one requirements document, for around $1,609 in AI spend across 5.5 days, producing 82 database models, 343 API endpoints, and roughly 454 automated tests, with a conventional git history any engineer can read back. On the fixed-budget MVP side, BRIO shipped as a working AI video-to-brief tool for $3,375, about 17% under estimate.

What type of SaaS is actually getting built

Even the software that keeps the "SaaS" label isn't the old horizontal dashboard. Looking at our 2026 Upwork lead categories outside the pure AI tag, the demand is heavily vertical: SaaS-labeled requests (153 leads), followed by healthcare (67), marketplace (33), e-learning (27), and ERP (24), each one a specific workflow for a specific industry, not a general-purpose tool.

Our own 2026 inbound requests confirm the same pattern at the project level. Recent briefs include a basketball scouting and player evaluation platform with custom scoring logic, a medical supply chain platform built around pharmaceutical traceability and regulatory compliance, a mobile-first B2B SaaS for trades contractors, and a fully specified niche accounting platform for the Ukrainian market. None of these are "a SaaS" in the generic sense. Each is a system built for one workflow, in one industry, often with compliance or domain-specific logic that a horizontal tool couldn't handle out of the box.

That's the practical version of "vertical beats horizontal": the SaaS still getting built in 2026 is narrower, more compliance-aware, and more workflow-specific than what shipped a few years ago, whether or not the founder calls it AI.

The delivery model that makes either path fast

None of this works if choosing the right shape costs you six extra months of build time. It shouldn't, and here's why.

We build software as an AI-native team: AI embedded at every layer of delivery, senior architects owning the structure on top of it. As our CTO Rodion Salnik describes the orchestrator behind Fielder, the system "sits somewhere in the middle between custom software development and software-as-a-service products. We don't code too much by our own, we just control and build based on the platform, and the platform actually generates the software." That middle ground is the point: not custom development at custom-development speed, and not a rigid SaaS template you have to bend your business around.

In practice this covers five paths, and the right one depends on the three checks above, not which word sounds better in a pitch: build a SaaS with AI functionality from day one, add AI into an existing SaaS as agents or a copilot, turn a SaaS into an agent that does the work, build a multi-tenant AI product with usage-based pricing (the Fielder shape), or turn a service into software you sell or run on. Most founders land on the first or fourth. Scaling teams with a live SaaS more often land on the second or third.

Your 10-minute self-check

Before you brief an agency or an investor, answer these three questions in one sentence each. No research required, just what's true right now.

- Positioning. In one sentence, is this a tool a person operates, or a system that does the work for one specific industry?

- Pricing. Would your ideal customer rather pay per seat, or per outcome? If you're not sure, ask what they'd cancel first if their bill doubled.

- Shape. List the three most valuable actions your product performs. For each one, does the software display information, or take the action itself?

If two or more answers point toward "does the work" and "outcome," you're building an AI-native product, whatever you end up calling it. If they point the other way, you're building a strong, focused SaaS, and that's still a real, growing business to build. Either answer is fine. Guessing wrong on architecture, and finding out eighteen months in, is the expensive mistake.

Whichever way your self-check comes out, the build doesn't have to be the slow part. If you want a second opinion on where your idea lands, Brocoders builds both shapes as an AI-native team, and our AI product development work is a good place to see what the "does the work" side actually looks like once it's shipped.

Frequently Asked Questions

No. Global SaaS spend is still projected to grow to about $576 billion by 2029. What's dying is one version of it: per-seat pricing on slow feature cycles that an AI agent can now replace directly, a shift Gartner puts at $234 billion of exposed spend by 2030.

A SaaS product is typically a tool a person operates. An AI product, in the vertical sense used here, does the work itself for one industry, usually priced on usage or outcome. Most real products sit between the two; the three checks above tell you where.

Run the self-check above. If your most valuable actions look like something an agent should do rather than display, and your customer would rather pay per outcome, build for that from day one. If not, a focused SaaS is still a legitimate, growing business, and Y Combinator's own 2026 batches show both paths still get funded.

Our own numbers: a fixed-budget AI MVP for $3,375, and a full vertical AI product (database models, API layer, automated tests included) for around $1,609 in AI spend across 5.5 days. Comparable traditional SaaS builds typically run into the tens of thousands.

Yes. Add AI into an existing SaaS as a copilot or agent, or re-architect one workflow so the AI does the work instead of a user clicking through it. Usually a scoped addition, not a full rebuild.

A product built for one industry, where AI performs the core work rather than assisting a human through a dashboard, usually priced on usage or outcomes instead of seats. Fielder is a working example.